Commercial Solutions

Minerva AI: Powering Profitable Growth for Small Commercial

Write More of the Right Business and Less of the Wrong

Growing a small commercial book is straightforward, but growing one profitably is the hard part. Commercial Solutions gives carriers the real-time commercial lines intelligence to do both, quoting faster on the risks worth writing, pricing more accurately on the ones that need it, and catching the adverse selection that erodes margin before it binds.

Built from 50 million+ small business profiles covering approximately 90% of all insurable small businesses in the U.S., it's the data layer that turns underwriting decisions into a competitive advantage.

Inside Minerva Explorer

Three Views, One Underwriting Picture.

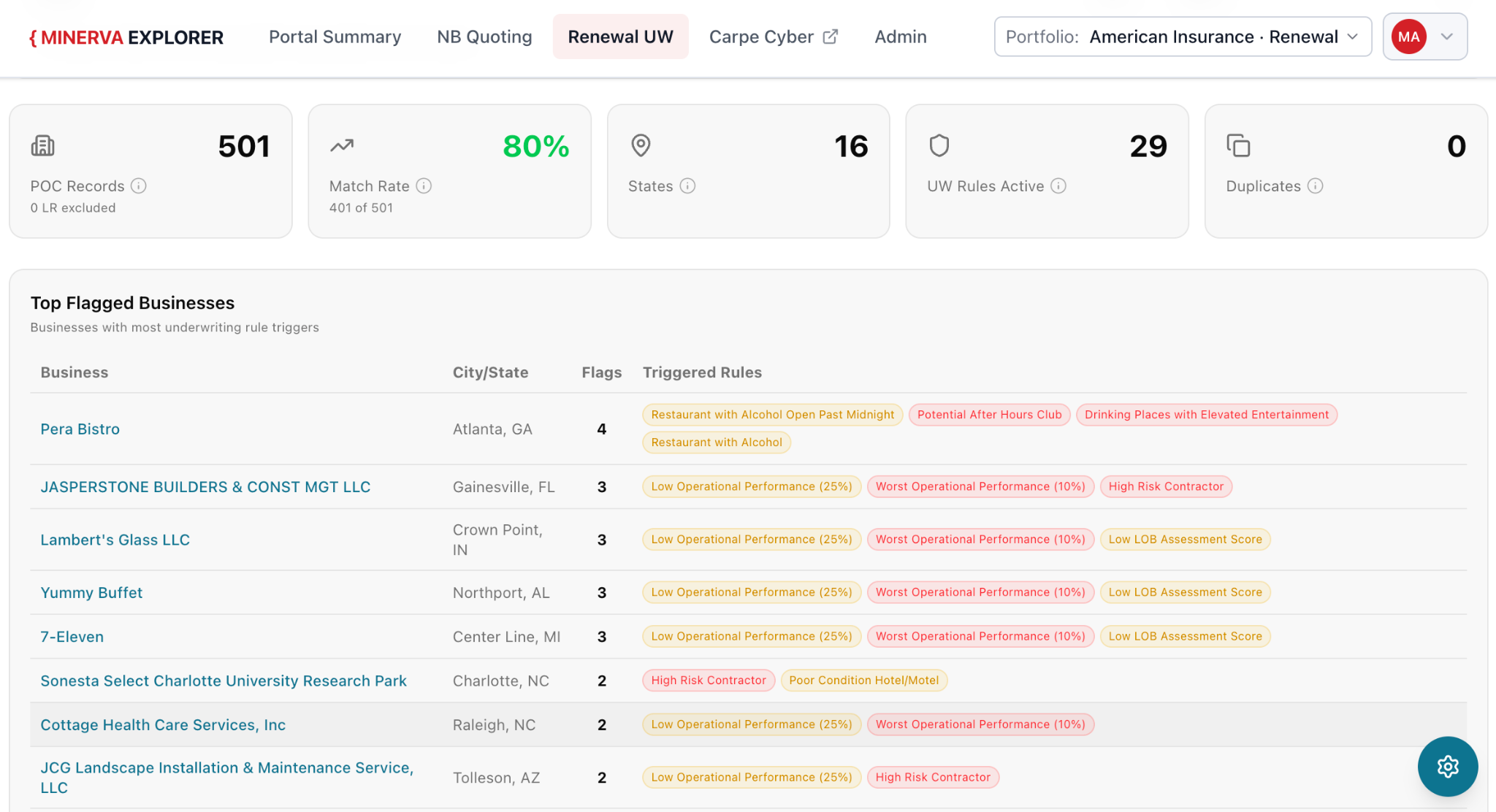

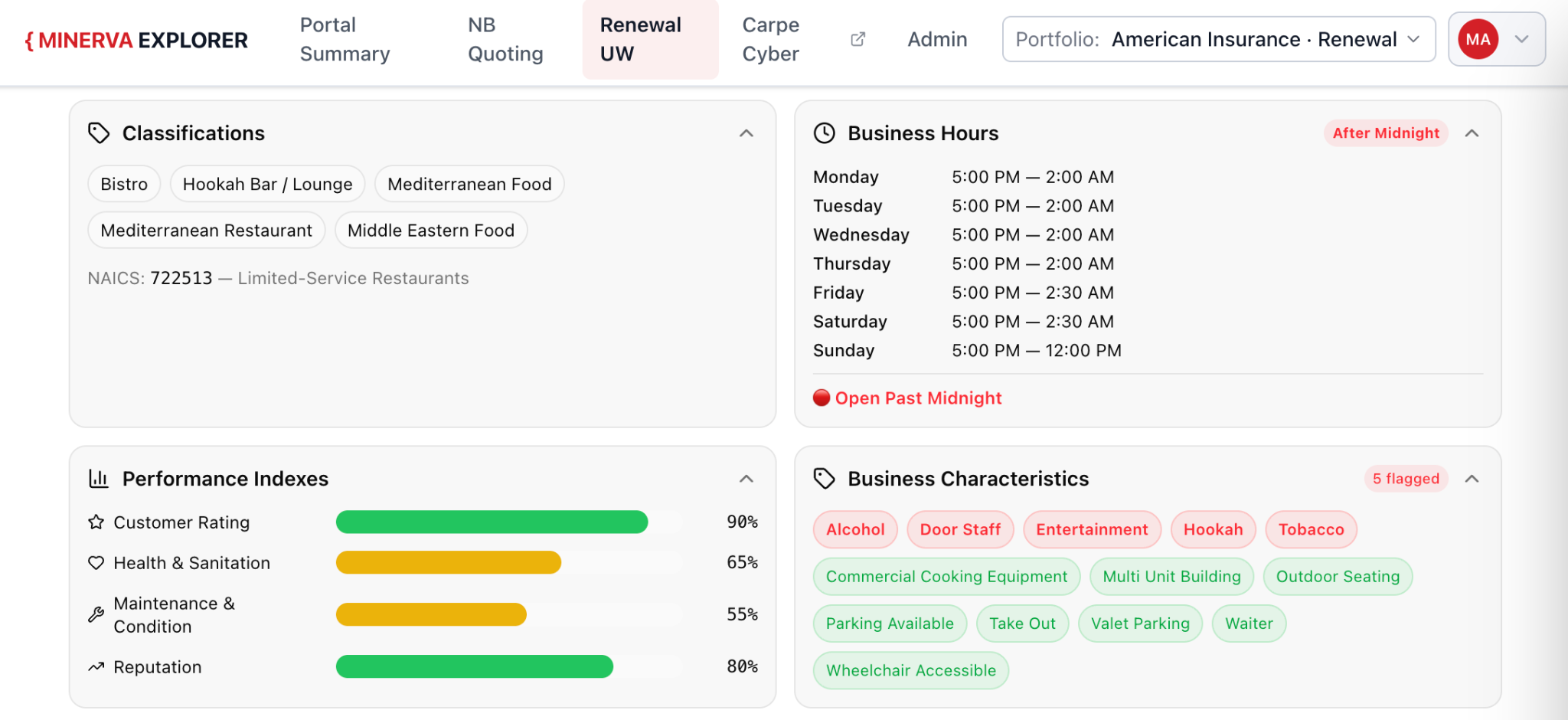

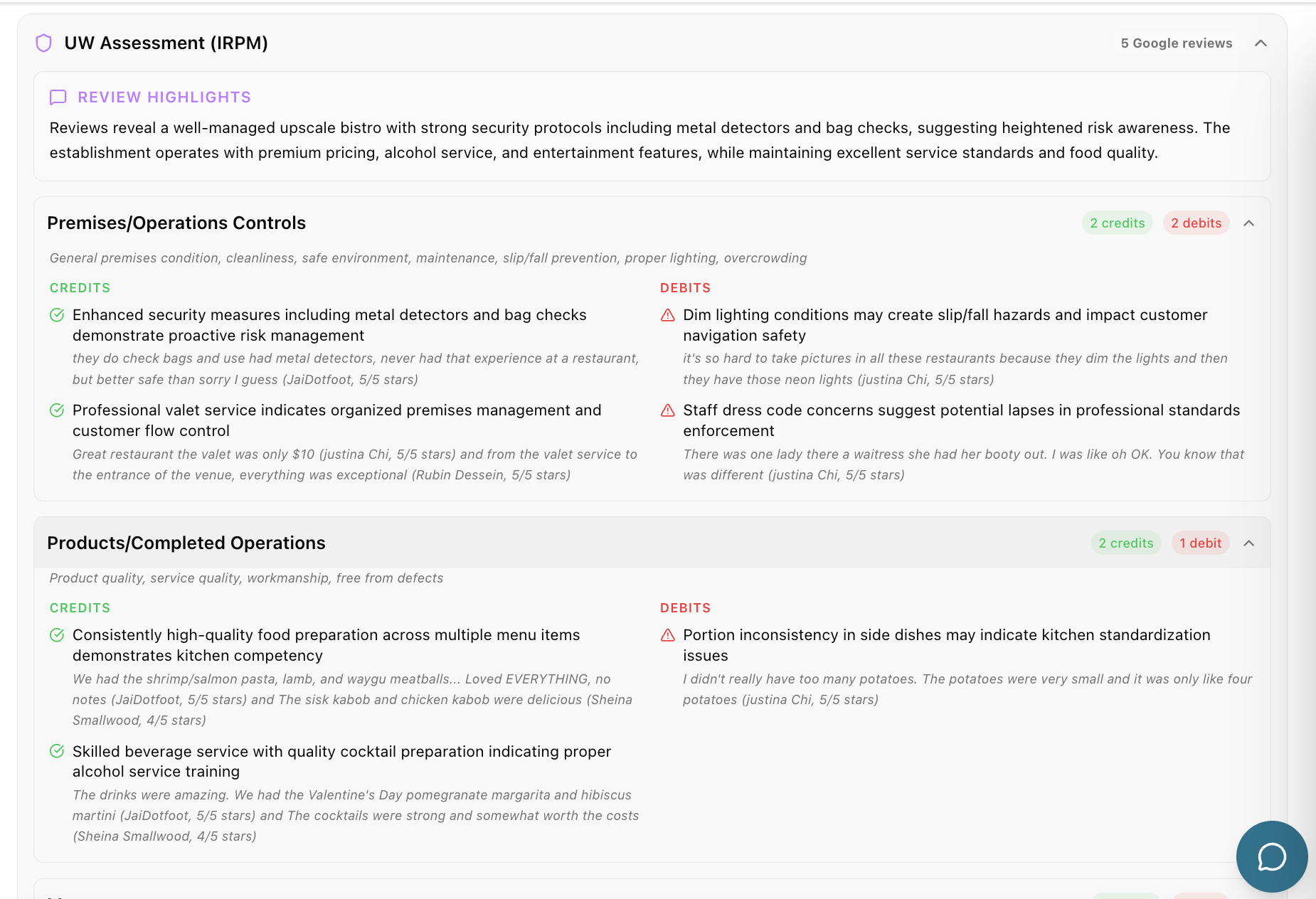

Tap a view to see exactly what underwriters see, from the portfolio-level renewal queue down to a single business profile and the IRPM assessment that lands on the file.

Renewal underwriting: portfolio match rate, flagged businesses, and the specific UW rules each triggered.

What Traditional Underwriting Data Misses

Small commercial underwriting runs on incomplete information. Static submissions, stale NAICS and SIC classifications, and businesses that evolve faster than carriers can keep up produce the issues that show up in every book review: misclassified operations that drive premium leakage, adverse selection from risks that looked fine on paper, and renewal portfolios where no one has time to confirm the business on file is still the business at the address. Firmographics, credit, and property data already sit inside everyone's pricing model, so they have stopped functioning as a differentiator.

Carpe builds continuously updated profiles of how small businesses actually operate, sourced from real-time online business data across 50 million+ small business profiles that cover approximately 90% of all insurable small businesses in the U.S. Those profiles translate into predictive scores, operational indicators, and AI insight that plug directly into quoting, triage, pricing, and renewal workflows, with reason codes and public-source evidence behind every signal so underwriting decisions stay consistent, explainable, and defensible.

The Results Carriers Are Seeing in Production

reduction in adverse selection

increase in straight-through processing

points of pricing model lift

loss ratio improvement

expense ratio reduction

return on investment

Results based on carrier production data across BOP, General Liability, Workers Compensation, and commercial property lines. Individual results vary based on book composition and implementation depth.

Two Modes, One Platform

Minerva runs in two modes that share the same data and the same scoring engine, so carriers can keep volume flowing through automation and still get deeper analysis on the risks that need it.

Mode

Minerva Instant

Risk signals and Carpe Risk Score in under a second, ready to embed in rating, triage, and straight-through processing.

Use it for: new-business triage, sub-second decisions, STP, and appetite screening at the point of quote.

Mode

Minerva Thinking

One to three minutes of deeper analysis on submissions that need real underwriting judgment, with match rates up to 25% higher than Instant alone.

Use it for: referrals, renewal reviews, batch pricing, and anywhere the rating engine alone isn't enough.

Carriers tune both modes to their own appetite, segmentation, and pricing strategy without writing code.

Behind every Minerva response sits a catalog of scores, indexes, and operational attributes drawn from 50M+ continuously updated small business profiles. See the full signal catalog →

Minerva at Every Stage of the Policy Lifecycle

Minerva doesn't stop working once a quote is bound. The same engine follows each policy from first submission through loss-ratio feedback, refreshing the picture every time the carrier needs it.

Step 01

Quote

Sub-second commercial intelligence and Carpe Risk Score flow into the rating engine on first submission, sharpening binding decisions the moment a quote arrives.

Step 02

Bind

Thinking-mode analysis runs on flagged risks before bind, pulling deeper operational and online signals into the file without slowing the workflow.

Step 03

Mid-Term

Minerva watches the bound book for material changes in business activity, web presence, and operational signal that would shift appetite or pricing.

Step 04

Renewal

Each renewal returns a refreshed picture of the risk and the score, with carrier-defined logic deciding which accounts get the deeper Thinking-mode review.

Step 05

Loss-Ratio Feedback

Outcomes feed back into Minerva so the models keep learning from how each carrier's book actually performs against the predictions Minerva produced.

Up and Running in Days, Without the IT Lift You'd Expect

Insurance IT teams are stretched thin, and integration timelines can stall even the best initiatives. Commercial Solutions reaches production fast, with flexible delivery options that work with the systems you already have.

All three options integrate with core systems in a matter of days, not months, so you're generating value before your next committee meeting.

For Carriers on Proprietary Platforms

Embed Minerva's Insights Into Your Own Platform

Carriers running on proprietary underwriting platforms can plug Minerva directly into their existing systems. Every score, index, attribute, and AI-generated insight is available through Minerva API, with the same data and reasoning engine that powers the Explorer cockpit.

For Data Science Teams

Building Your Own Models?

Commercial Solutions data is available for licensing. If your actuarial or data science teams are building proprietary commercial lines pricing models, segmentation engines, or AI-powered underwriting workflows, we can discuss how to put 50 million+ small business profiles and years of scored, structured online data to work inside your own systems, including as training data for AI models and decision-layer enrichment.

Testimonials

What Carriers Say About Carpe.

“By integrating new data elements from Carpe Data into our insurance programs for small businesses, we can better understand the challenges faced by business owners and identify options to address their commercial insurance needs.”

Sharon Fernandez · Farmers Insurance

President of Business Insurance

“Carpe Data is the latest addition to Zurich’s ongoing innovation programs focused on transforming the future of insurance…[Carpe Data] supports Zurich’s ongoing efforts to improve the claimant experience by expediting low-risk claims, and by providing new insights to help our people make informed, accurate, and timely decisions.”

Scott Clayton · Zurich Insurance Company Ltd

Head of Claims Fraud, UK

“Carpe Data has been a great partner in helping us strengthen the claims handling process…Online Injury Alerts helps [us] continue to meet our goals of increased efficiency, reduced potential fraud and improved customer experiences.”

Douglas L. Kratzer · The Hanover Insurance Group

Vice President, Claims

Common Questions About Commercial Solutions

Answers to the questions carriers ask most often about data, integration, and what Commercial Solutions finds that other sources don't.

What types of commercial lines data does Commercial Solutions provide?+

Commercial Solutions returns risk scores, business characteristics, NAICS/SIC classification validation, loss propensity scores, anomaly scores, hours of operation, and AI-generated business summaries, all sourced from online business data across 50 million+ continuously updated small business profiles. Insights are available via sub-second API, searchable portal, or batch scoring for actuarial and book review work.

How does Commercial Solutions reduce adverse selection in commercial underwriting?+

Commercial Solutions surfaces hidden business operations, misclassified exposures, and high-risk characteristics that self-reported application data misses. By screening submissions against your appetite guidelines and flagging anomalous or atypical operations before bind, carriers using Commercial Solutions have reduced adverse selection by up to 40% and improved loss ratios by 1.5 points.

What is the difference between Minerva Instant and Minerva Thinking?+

Minerva Instant is built for speed. It returns risk signals from our datastore in under one second, making it ideal for new business triage, straight-through processing, and pricing at submit. Minerva Thinking is built for depth, combining the datastore with live online search and AI-powered analysis to return results in one to three minutes for referred quotes, renewals, and cases where an underwriter needs more context.

How quickly can Commercial Solutions integrate with our systems?+

Commercial Solutions is built for fast implementation across every delivery option. The sub-second REST API integrates with quoting, triage, and pricing systems in a matter of days, the searchable portal requires no IT lift at all, and batch scoring can be set up and running within a week, so most carriers are generating value before their next committee meeting.

What makes Commercial Solutions different from traditional commercial underwriting data providers?+

Most traditional data providers rely on firmographic, credit, and property data that has already been priced into the market. Commercial Solutions adds a differentiated layer: real-time online business data sourced from company websites, review platforms, social media, and commercial sites, the signals that tell you what a business actually does, not what it reported on the application. That is why our data adds 10+ points of model lift on top of traditional datasets, not instead of them.

Is Commercial Solutions data available for AI model training and pricing model development?+

Yes, Commercial Solutions data is available for licensing by actuarial and data science teams building proprietary commercial lines pricing models, segmentation engines, or AI-powered underwriting tools. We can structure access to our full 50 million+ small business profile dataset, scored attributes, and historical online signals based on your specific use case. Contact our commercial risk team to discuss data licensing terms, scope, and integration options.

See How Carriers Are Growing Their Books Profitably

Whether you're looking to increase flow, sharpen segmentation, reduce loss ratio, or clean up a renewal book, our commercial risk team can walk you through sample results for your classes of business and show you what Commercial Solutions finds that other commercial underwriting data sources don't.